Debt collectors in the UK chase money for outstanding debts owed.

If you are being chased by a debt collection agency in the UK you want to know all the rights you have.

We strongly advise before speaking to debt collectors you speak to a debt advisor for free who can assist on what your solutions are.

Find Out The Best Debt Solution Bespoke To Your Financial Situation

30 Second Debt Assessment QuizSome debt advisors might be able to assist you in legally writing off 85% of your debts if you qualify.

Table of Content

- 1 Why Are Debt Collectors Chasing You?

- 2 What Are Debt Collectors Not Allowed To Do?

- 3 Do Not Pay Debt Collectors Until You Get Advice

- 4 How do I deal with debt collectors?

- 5 What happens if you ignore debt collectors UK?

- 6 Can I refuse to deal with a debt collection agency?

- 7 How long can debt collectors chase you for UK?

- 8 Can debt collectors refuse my payment plan?

- 9 Can a debt collection agency take me to court?

- 10 How can debt collectors find me?

- 11 What rights do debt collectors have?

- 12 List of Debt Collection Agencies UK

- 13 The Journey of Debt

Why Are Debt Collectors Chasing You?

Debt recovery firms chase you in one of two cases:

- A creditor has employed a debt collector to chase monies outstanding on their behalf

- A creditor has sold your debt to them

In both cases it is important you know your rights and what debt collectors are allowed to do.

What Are Debt Collectors Not Allowed To Do?

Debt collectors are not allowed to do the following:

- Contacting you on social media – they are strictly forbidden to contact you on Facebook, Instagram, Twitter or social profiles.

- Contact you at work – no debt collector is allowed to contact you at your workplace.

- Reveal debts to others – some debt recovery companies try to embarrass you and put you under more pressure by speaking to others at the workplace or on the home telephone but they are not allowed to reveal your circumstances to others.

- Chase you outside of specified hours – debt collectors can only contact you between the hours of 8am and 9pm during the week and not at the weekend or on bank holidays.

- Make additional charges – under debt collection guidance the maximum a debt collector can add is 8%. Any debt collection firm trying to add more than 8% is simply not allowed to do so.

- Give misleading information – chasing the debts some debt collectors will try to threaten court action or lie to add fear into you to pay. Report this to the FCA as it is simply forbidden for them to do so.

- Pressure you to pay today – you should never be pressurised, the debt collector has to work within what is affordable for you and what’s realistic for you to repay.

Do Not Pay Debt Collectors Until You Get Advice

Check out this video which explains the 8 things debt recovery companies in the UK are not allowed to do.

How do I deal with debt collectors?

The best way to deal with debt collectors is to cooperate with them as much as you can. Trying to sweep the situation under the rug and run away from it generally makes it worse.

Many people have said they have been contacted by numbers they do not know, such as 01415704152, therefore, they will not answer.

It’s important to make sure that the debt you’re being contacted about is actually yours. Once you’ve established that it is your responsibility, you can get help from a debt advice service and cooperate with the debt collectors to reach an agreement.

Remember that debt collectors do not have to power to forcibly enter your home or to pressure you into paying more than you can afford to.

What happens if you ignore debt collectors UK?

It’s never a good idea to ignore debt collectors, no matter the circumstances. Ignoring them won’t stop them trying to contact you, even if you believe the debt is not yours to pay.

If the debt is yours to pay, it’s even more of a problem if you ignore the debt collectors. This can give them a reason to enforce more serious action on you. It can also increase the debt you already owe by adding interest and additional charges.

It is best to take control of the situation, seek help from a debt expert and get the situation dealt with.

Did You Know You Can Write Off Up To 85% Of Your Debts?

Do I Qualify?Can I refuse to deal with a debt collection agency?

No, you can’t refuse to deal with a debt collection agency.

This will only make the situation worse, potentially increasing your debt and leading to further action being taken. The best thing to do is to deal with your debt problems by getting advice from a professional.

How long can debt collectors chase you for UK?

In most cases, debt collectors in the UK can chase you for six years. However, there are some types of debt, such as mortgages, where the limit extends to 12 years.

These limitation periods have certain rules in place in order for them to be upheld. If you make a payment towards your debt or even acknowledge it in writing, this will reset the limitation period.

If your creditor has not contacted you in six years, your debt will become unenforceable.

Can debt collectors refuse my payment plan?

Yes, debt collectors do have a right to refuse your payment plan.

In most cases, the debt collection agency will be working on behalf of the creditor you actually owe money to. So, the decision to refuse your payment plan will ultimately lie with them.

If debt collectors or creditors do decide to refuse your chosen payment plan, it’s a good idea to get in touch with a debt help service. They can contact the collection agency or creditors on your behalf to discuss the repayment.

Interested In Finding Out More About The Debt Solutions Available?

Find Out MoreCan a debt collection agency take me to court?

It is possible that a debt collection agency could take you to court if they are the legal owner of your debt. If they are just working on behalf of your creditor, it would be the creditor’s decision to take you to court.

Going to court is usually used as a last resort when all other options have been exhausted and the debt collectors feel there is no other way to get you to pay the debt.

If you think that a debt collection agency is planning to take you to court, the best thing to do is seek debt advice from a professional service. They can help you set up a repayment plan to get your debts under control, and then discuss this with your creditors on your behalf.

How can debt collectors find me?

There are a number of ways that debt collectors can find and make contact with you. One of the main methods would be checking your credit report. This will have your basic contact details and might also show your address.

They could also check government databases or contact government agencies which might have your details. In some cases, you might have submitted your information in an online form or survey, which debt collectors can then access as a third party.

What rights do debt collectors have?

Some of the practices that debt collectors employ may seem excessive, but they do have the right to do them. You can’t stop a debt collector from making contact with you if the debt they are chasing is legitimately owed.

However, they are not permitted to discuss the debt with anyone but you. They also can’t intimidate you or give you false information in an effort to get you to pay. If you suspect a debt collector is doing something that’s not allowed, you should report them.

List of Debt Collection Agencies UK

Here is a list of all the debt collectors in the UK.

- Attachment of Earnings Order

- Debt Collectors

- Direct Earnings Attachment

- How to Deal With Bailiffs

- Solicitors Letter Before Action

- Solicitors Letter threatening Court Action for Debts

- The Ultimate Guide to ABC Debt Recovery

- The Ultimate Guide to Advantis Credit Debt Recovery

- The Ultimate Guide to Akinika Debt Recovery

- The Ultimate Guide to Aktiv Kapital Debt Collectors

- The Ultimate Guide to Andrew James Enforcement Ltd

- The Ultimate Guide to Anglian Water Debt

- The Ultimate Guide to ARC Europe Ltd Debt Collectors

- The Ultimate Guide to ARP Enforcement Agency

- The Ultimate Guide to Arrow Global Debt Collectors

- The Ultimate Guide to Arvato Financial Solutions

- The Ultimate Guide to Asset Collections and Investigations (ACI)

- The Ultimate Guide to Asset Link Capital

- The Ultimate Guide to Barclaycard Debt

- The Ultimate Guide to Barclays Debt Collection

- The Ultimate Guide to Blackhorse Financial

- The Ultimate Guide to Bluestone Credit Management

- The Ultimate Guide to BPO Collections

- The Ultimate Guide to Bristow and Sutor Debt Collectors

- The Ultimate Guide to BT Debt Collection

- The Ultimate Guide to Buchanan Clark & Wells Debt Collectors

- The Ultimate Guide to Cabot Financial

- The Ultimate Guide to Capital Resolve

- The Ultimate Guide to CapQuest Debt Recovery

- The Ultimate Guide to CCS Collect Debt Collectors

- The Ultimate Guide to Chandlers Enforcement Agents

- The Ultimate Guide to CL Finance Debt Collectors

- The Ultimate Guide to CLI International Debt Collectors

- The Ultimate Guide to Cobra Financial Solutions

- The Ultimate Guide to Confero Collections Ltd

- The Ultimate Guide to Constant & Co

- The Ultimate Guide to County Court Business Centre

- The Ultimate Guide to Court Enforcement Services Ltd

- The Ultimate Guide to CPER Bailiffs

- The Ultimate Guide to Creation Financial Services

- The Ultimate Guide to CRS Debt Collectors

- The Ultimate Guide to DCBL

- The Ultimate Guide to Debt & Revenue Services

- The Ultimate Guide to Debt Guard Solicitors

- The Ultimate Guide to Debt Managers Services Ltd

- The Ultimate Guide to Debt Squared Debt Collection

- The Ultimate Guide to DG Collection Services Ltd

- The Ultimate Guide to Direct Legal Collections Debt Collectors

- The Ultimate Guide to Droyds Debt and Collection Services

- The Ultimate Guide to Dukes Bailiffs Ltd

- The Ultimate Guide to DVLA Debt Collection

- The Ultimate Guide to eBay Debt Collection

- The Ultimate Guide to EE Debt Collection

- The Ultimate Guide to Elliot Davies High Court & Civil Enforcement

- The Ultimate Guide to Engage Services Debt Collection

- The Ultimate Guide to EOS Solutions Debt Collectors

- The Ultimate Guide to Equita Ltd Debt Collectors

- The Ultimate Guide to EUI Ltd Debt Collection

- The Ultimate Guide to Excel Civil Enforcement

- The Ultimate Guide to Fredrickson Financial

- The Ultimate Guide to FSB Debt Recovery

- The Ultimate Guide to GKM Group Ltd Debt Collectors

- The Ultimate Guide to Gladstones Solicitors

- The Ultimate Guide to Global Debt Recovery

- The Ultimate Guide to Goodwillie & Corcoran

- The Ultimate Guide to GTM Debt Recovery Services Ltd

- The Ultimate Guide to High Court Enforcement Group

- The Ultimate Guide to Hillside Services Debt Collection

- The Ultimate Guide to Hoist Finance

- The Ultimate Guide to Hoist Portfolio Holding Ltd

- The Ultimate Guide to IMFS Debt Collection

- The Ultimate Guide to Indigo Michael

- The Ultimate Guide to Intrum Justitia

- The Ultimate Guide to Irwin Mitchell Debt Collectors

- The Ultimate Guide to Jack Russell Debt Collection

- The Ultimate Guide to Jacobs Enforcement

- The Ultimate Guide to JBW Debt Collectors

- The Ultimate Guide to Jefferson Capital International

- The Ultimate Guide to JTR Collections

- The Ultimate Guide to Judge and Priestley

- The Ultimate Guide to KPR Debt Collection

- The Ultimate Guide to Lantern Debt Collectors

- The Ultimate Guide to LCS Debt Recovery

- The Ultimate Guide to Lending Stream LLC

- The Ultimate Guide to Lightfoots Debt Recovery

- The Ultimate Guide to Link Financial Debt Collectors

- The Ultimate Guide to Lowell Group Debt Recovery

- The Ultimate Guide to Mackenzie Hall Debt Collectors

- The Ultimate Guide to Marston Group Ltd Debt Collectors

- The Ultimate Guide to Max Recovery Limited

- The Ultimate Guide to MKDP Debt Collection

- The Ultimate Guide to Moorcroft Debt Recovery Ltd

- The Ultimate Guide to Moriarty Law

- The Ultimate Guide to Mortimer Clarke Solicitors

- The Ultimate Guide to My Jar Debt Collectors

- The Ultimate Guide to Natwest Debt Collection

- The Ultimate Guide to NCO Financial Services

- The Ultimate Guide to Newlyn PLC Debt Collectors

- The Ultimate Guide to Northern Debt Recovery

- The Ultimate Guide to Npower Debt Collectors

- The Ultimate Guide to One Source Debt Resolution

- The Ultimate Guide to Opos Limited

- The Ultimate Guide to Optima Legal

- The Ultimate Guide to Orbit Debt Collection

- The Ultimate Guide to Oriel Debt Collection

- The Ultimate Guide to P&J Debt Collection

- The Ultimate Guide to Phoenix Commercial Collections

- The Ultimate Guide to PRA Group

- The Ultimate Guide to Proserve Debt Recovery & Bailiff Service Ltd

- The Ultimate Guide to QDR Solicitors

- The Ultimate Guide to Resolve Call Debt Collectors

- The Ultimate Guide to Restons Debt Collectors

- The Ultimate Guide to Reventus Enforcement Agents

- The Ultimate Guide to Richburns

- The Ultimate Guide to Robinson Way

- The Ultimate Guide to Ross & Roberts Enforcement Agents

- The Ultimate Guide to Rossendales Debt Collectors

- The Ultimate Guide to Rundles

- The Ultimate Guide to Scotcall Debt Collecting Services

- The Ultimate Guide to Scott and Co

- The Ultimate Guide to Scottish Power Debt Collectors

- The Ultimate Guide to Shoosmith Debt Collectors

- The Ultimate Guide to Sigma Red Debt Collectors

- The Ultimate Guide to Solex Legal Services

- The Ultimate Guide to Spratt Endicott Debt Recovery

- The Ultimate Guide to STA International

- The Ultimate Guide to Sterling Debt Recovery

- The Ultimate Guide to Stirling Park Debt Collectors

- The Ultimate Guide to Swift Group Debt Collectors

- The Ultimate Guide to The Ultimate Guide to Past Due Credit Solutions Ltd (PDCS)

- The Ultimate Guide to Thomas Higgins Partnership

- The Ultimate Guide to Top Service

- The Ultimate Guide to Trace Debt Recovery

- The Ultimate Guide to TV License Debt Collection

- The Ultimate Guide to UK Search Limited (UKSL)

- The Ultimate Guide to Vodafone Debt Collection

- The Ultimate Guide to Walker Love

- The Ultimate Guide to Wescot Credit Services Ltd

- The Ultimate Guide to Whyte & Co

- The Ultimate Guide to Wilson & Roe High Court Enforcement Ltd

- The Ultimate Guide to Zenith Debt Recovery

- The Ultimate Guide to Zinc Debt Collection

- What Cant Bailiffs Take

- Who Called Me

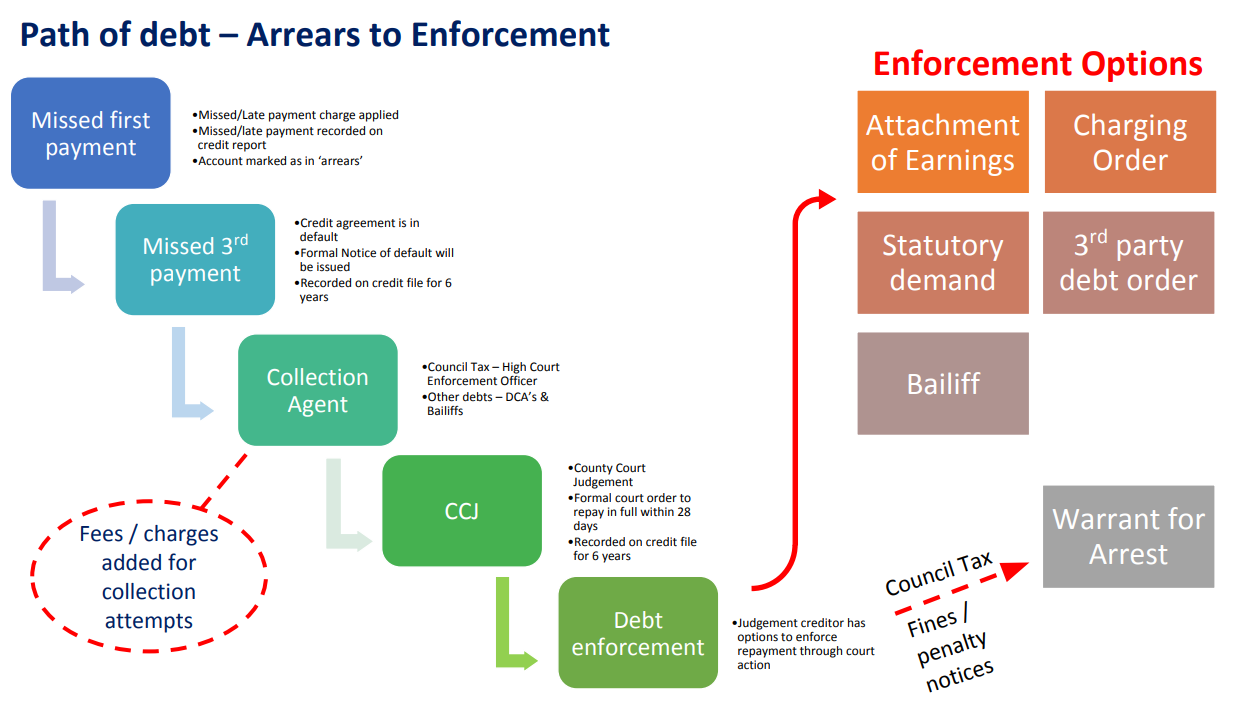

The Journey of Debt

Here is the path of debt – from arrears to enforcement.

- Missed First Payment – Marked as in ‘arrears’

- Missed 3rd Payment – Formal Notice of Default

- Collection Agent

- CCJ – County Court Judgement

- Debt Enforcement – Attachment of Earnings

- Debt Enforcement – Charging Order

- Debt Enforcement – Statutory Demand

- Debt Enforcement – Warrant for Arrest

- Debt Enforcement – 3rd Party Debt Order

- Debt Enforcement – Bailiff